Other than our regular trips between Kerikeri and Auckland, the winter and early spring months have been devoid of other adventures. That is not to say that life has been boring.

With interest rates continuing their steady journey south, towards zero or negative territory, and our Reserve Bank Governor telling us we need to spend in order to keep the economy buoyant, we started looking at other options. As an aside, maybe it is a case of the current economic model that needs reviewing, i.e., economies cannot continue growing when we live on a planet with finite resources, or can they? Maybe if the country started to get real about the ever increasing (future) cost of sticking our heads in the sand over the changing climate and started doing something, the Governor would get more growth than he could handle. We won’t hold our breath on that happening until the proverbial hits the fan.

For us, the primary objectives of saving was; to have a nest egg to generate an income in our retirement, cover additional health and care costs, keep a dry roof over our heads and maybe throw in a bit of travel. While we did the latter for a while, our carbon conscience started to prick us and we dramatically scaled back on that.

Sure we could switch to higher yielding investments but I was always lead to believe that yield reflects risk and currently, things look more than a little overcooked (relative to reality) and markets are probably due for a sizable ‘correction’. Based on the last ‘correction’ in 2008, it won’t be the big guys who suffer. Our ‘sunset years’ are not the time we want to be starting over (again). Time for Plan B (not to be confused with Planet B which I believe is mythical).

When we were younger, the alternative to saving, was to pay off the mortgage faster but with rates at current levels I am not sure that rule of thumb still applies. In our dotage, maybe, an alternative to interest income, is to reduce your living costs. As investment gurus will tell us, we need to have a balanced portfolio, but I guess it doesn’t all need to be in investments that generate commissions for them.

With that personal odometer rising almost as quick as atmospheric carbon readings, the first rule to forget is the number of years required to recoup your investment. At our age, cash flow is now king. What we are looking for is an immediate impact on the number of dollars available to cover our expected annual living costs. Maybe we should invest in our own infrastructure in order to balance the portfolio.

Because we have been running up so many kilometers in our car (about 16,000k per year), switching to an electric vehicle was a no-brainer. Not only did it reduce our expenditure on fuel and maintenance by several thousand dollars annually, it has had a great side effect of reducing our carbon emissions. Save money and the planet, a true win win. The savings in fuel and maintenance and the elimination of tax on investments returns, would require the equivalent of an 8.5% return for a bank deposit. Today’s ‘great rates’ being offered by one of our banks, are around 2.6% (less withholding tax) for anything between 3-12 months with a minimum investment of $10k.

However, don’t rush off and buy an EV just yet, read on. If we were not travelling the distances that we currently are, the equivalent rate of return on the EV would reduce. We would still have the savings compared to our baseline budget that included the internal combustion engined car, but those savings would no longer all be attributable to an EV, part relates to our reduced use of a car. If you don’t use a car much, then it is probably best to ditch it. No point in paying insurance and on road costs for nothing.

I know that a car depreciates in value and your underlying investment becomes worthless but, we can’t take that underlying investment with us into an afterlife. Our plan is to not replace the car if this one sputters out before us so let’s call the ‘investment’ a sunk fund.

What else could we do to maintain our spending power?

We added an array of eight solar panels to our roof 2 years ago. It was to be a test of the solar option which would allow us to get a better understanding of how generating some of our own power could work for us. My knowledge of electricity was abysmal at that stage but I did a crash course (Google) to ensure that I did not get sold a lemon. Our findings after 2 years, are that the benefits of solar are dependent upon the household. There is no size-fits-all solution. What we did has worked for us but I would not blindly recommend the same approach to others.

When we are at home we are using the power during the day which is important if you are just putting solar panels on your roof. You need to use as much of the power as you can while the sun is shining. Despite being away from home for nearly three months of the year, we achieved a 54% reduction in our power costs which translated to a return 8.3% that would have been needed from an equivalent bank deposit.

Solar does not deliver the same win win as an EV though, well in NZ. Here roughly 85% of our power is already from renewable sources so you are largely replacing renewable with renewable. While you are saving money, the planet saving is far more modest, so hold back on your ‘planet saving’ boasts. Having said that, the whole planet saving thing is probably going to have an impact on our future returns (if we hang around a little longer) as the country is ultimately forced to switch away from fossil fuel to electricity. While I read about the plans to move industry and transport to electricity, I don’t read much about plans for imminent infrastructure builds to provide for that additional electricity demand. The lag between demand and capacity would suggest that electricity price increases will be a sure bet. Gosh, we may even get paid a little more for our excess capacity but don’t factor that into your calculations just yet.

Could we squeeze more out of our solar system?

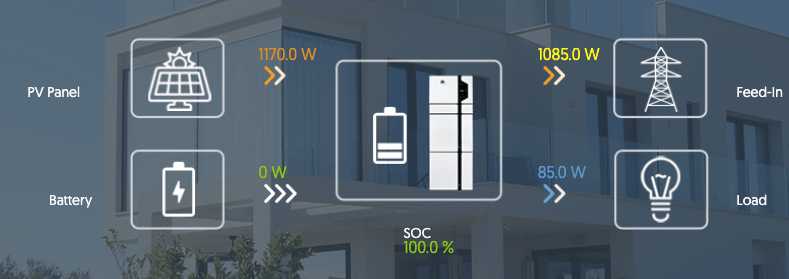

Our current setup is modest and, despite using as much power as we can while the sun shines (a bit like making hay while…), we were only using 57% of our solar production. The rest goes back to the grid earning $0.08c per kilowatt – we pay $0.422 per kilowatt for power from the grid. The only viable option was to dip our toes into power storage, in other words move to setting up our own little power company.

As with our first move, we preferred to test the water, add a limited amount of storage and a few more panels. I now had data to work with and as a result of driving an EV, better understood the area of battery storage. It was clear from my number crunching that in order to go off-grid, we would have to go with a system that was very expensive and, for a large part of the year, would generate too much power for our needs. At the current buy-back rates for power sent to the grid ($0.08), the returns on such a system barely competed with the abysmal deposit rates. By playing around with the variables, the optimal solution was to be the addition of four more panels and a modest 5.7kwh battery. This would make us grid free for roughly 9 months of the year and generate a return on the additional infrastructure equivalent to 5% from a bank term deposit.

We have taken the plunge and are now up and running with our little power company, in grid-free mode, at least until late April next year. A small bonus is that we will now have power for essential appliances if the grid goes down. While that was not a mandatory requirement for us, it may become more important if that additional grid capacity does not eventuate in time to meet the inevitable increased demand.

Tweaking our game plan is working for now but who knows what the future holds, apart from the obvious.

great story! and who was the lucky supplier of your battery? Inge

LikeLike

Husbands of course

LikeLike

Hubands – oh how I hate predictive text

LikeLike